Corporate bonds serve as a means for corporations to raise capital and for investors to earn returns while diversifying their portfolios. In this guide, we will cover major features of corporate bonds, exploring their characteristics, mechanics, risks, and benefits.

What are Corporate Bonds?

Corporate bonds are debt securities issued by corporations to raise funds for various purposes, such as financing operations, funding expansions, or refinancing existing debt. When investors purchase corporate bonds, they essentially lend money to the issuing company in exchange for regular interest payments and the eventual return of the principal amount at maturity.

Unlike government bonds, which are issued by sovereign entities, corporate bonds are issued by corporations across different industries and sectors. These companies range from established multinational corporations to smaller, growth-oriented firms. Corporate bonds come in various forms, including investment-grade bonds issued by financially stable companies and high-yield bonds, often referred to as “junk bonds,” issued by companies with lower credit ratings and higher risk profiles.

Characteristics of Corporate Bonds

Corporate bonds possess several key characteristics:

- Coupon Rate: The coupon rate represents the annual interest rate paid by the issuing corporation to bondholders. It is typically expressed as a percentage of the bond’s face value and determines the periodic interest payments investors receive.

- Maturity Date: The maturity date indicates the date on which the issuing company must repay the principal amount to bondholders. Corporate bonds can have varying maturity periods, ranging from a few months to several decades.

- Credit Rating: Credit rating agencies assess the creditworthiness of bond issuers and assign credit ratings based on factors such as financial stability, debt levels, and business prospects. These ratings provide investors with insights into the risk associated with investing in corporate bonds.

- Callability: Some corporate bonds include a provision that allows the issuer to redeem or “call” the bonds before their scheduled maturity date. Callable bonds provide issuers with flexibility but may result in early repayment for investors, potentially impacting returns.

- Yield: The yield of a corporate bond reflects the return on investment based on its coupon payments and market price. Yield varies inversely with the bond’s price, meaning that as the bond’s price rises, its yield decreases, and vice versa.

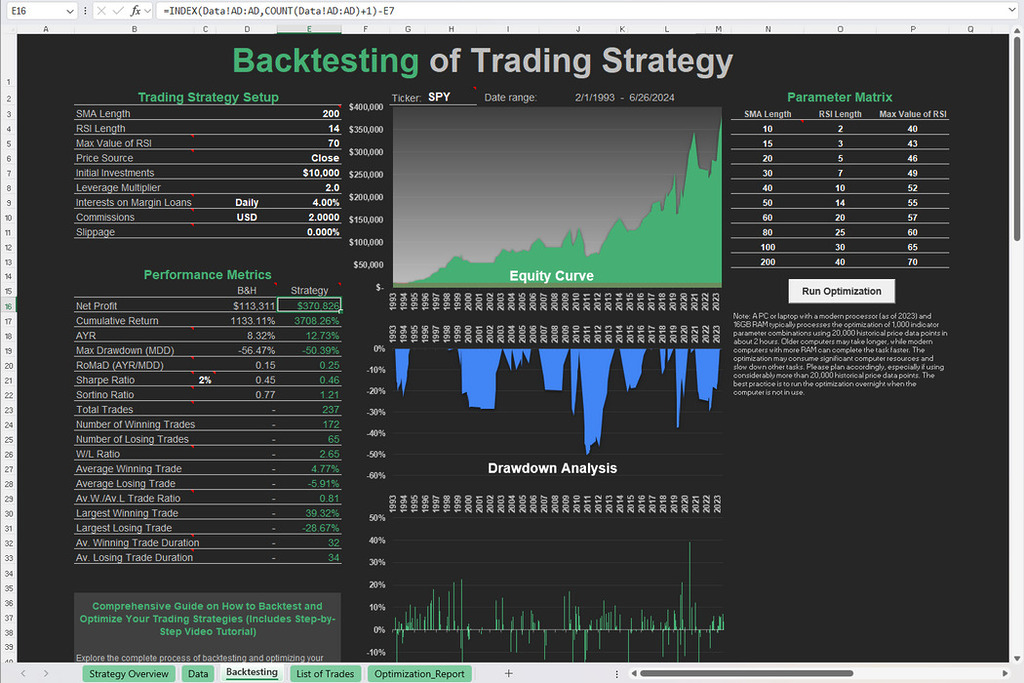

Free Backtesting Spreadsheet

Mechanics of Corporate Bond Issuance

The issuance of corporate bonds involves several key steps. Initially, the issuing corporation collaborates with investment banks or underwriters to structure the bond offering, determining essential terms such as the coupon rate, maturity date, and total issue size. Subsequently, thorough due diligence is conducted to assess the company’s financial health, market position, and creditworthiness, which helps determine the appropriate credit rating and pricing for the bonds.

Following issuance, bonds may be listed on stock exchanges or traded over-the-counter (OTC), providing liquidity and transparency for investors and facilitating secondary market trading. Issuing corporations are obligated to provide regular financial disclosures and updates to bondholders, ensuring transparency and accountability throughout the bond’s lifecycle. This ongoing reporting ensures that investors remain informed about the issuer’s financial health and performance, enhancing investor confidence and trust in the bond.

Types of Corporate Bonds

Corporate bonds can be categorized based on various criteria, including:

Investment-Grade Bonds

Investment-grade bonds are issued by financially stable companies with high credit ratings, typically BBB- or higher by major credit rating agencies. These bonds are considered relatively safe investments, with lower default risk compared to lower-rated bonds. Investment-grade bonds offer lower yields than lower-rated bonds but provide greater safety and stability for investors seeking steady income and capital preservation. These bonds are suitable for conservative investors.

High-yield bonds offer higher yields to compensate investors for the increased risk, making them attractive for income-oriented investors seeking higher returns.

High-Yield Bonds (Junk Bonds)

High-yield bonds, also known as junk bonds, are issued by companies with lower credit ratings or higher levels of financial risk. These bonds are typically rated below investment-grade (BB+ or lower) by credit rating agencies, indicating a higher risk of default. High-yield bonds offer higher yields to compensate investors for the increased risk, making them attractive for income-oriented investors seeking higher returns. However, they are more susceptible to default and market volatility, requiring careful credit analysis and risk management. High-yield bonds are suitable for investors with higher risk tolerance and seeking potential capital appreciation.

Convertible Bonds

Convertible bonds give bondholders the option to convert their bonds into a predetermined number of common stock shares of the issuing company. These hybrid securities offer investors the potential for capital appreciation if the issuer’s stock price rises, as well as the downside protection of a bond’s fixed-income stream. Convertible bonds typically have lower coupon rates than traditional bonds to compensate for the conversion feature. These bonds are attractive to investors seeking exposure to both fixed-income and equity markets, providing flexibility and potential upside potential.

Floating Rate Bonds

Floating rate bonds feature variable interest rates that adjust periodically based on changes in a reference rate, such as the London Interbank Offered Rate (LIBOR) or the prime rate. These bonds offer protection against interest rate risk, as their coupon payments fluctuate with prevailing market rates. Floating rate bonds are suitable for investors concerned about rising interest rates and inflation, as they provide a hedge against changes in interest rates. These bonds are commonly issued by financial institutions, governments, and corporations seeking flexibility in managing interest rate exposure.

Perpetual Bonds

Perpetual bonds have no fixed maturity date and pay periodic interest indefinitely, making them similar to equities in some respects. These bonds provide issuers with perpetual financing and flexibility, as they are not obligated to repay the principal amount to bondholders. Perpetual bonds offer investors the potential for stable income over an extended period, although they may include call options allowing the issuer to redeem the bonds under certain conditions. These bonds are commonly issued by financial institutions and utilities seeking long-term capital without the obligation of repayment.

By investing in a Corporate Bond ETF, investors gain exposure to a broad range of corporate bonds reducing the impact of individual bond defaults or credit events.

Corporate Bond ETFs

Corporate Bond ETFs are investment funds that pool investors’ money to invest in a diversified portfolio of corporate bonds. These ETFs are traded on stock exchanges like individual stocks, allowing investors to buy and sell shares throughout the trading day at market prices. By investing in a Corporate Bond ETF, investors gain exposure to a broad range of corporate bonds without the need to purchase individual bonds directly. Investors can spread their risk across hundreds or even thousands of bonds, reducing the impact of individual bond defaults or credit events. This diversification enhances portfolio stability and mitigates risk.

Transparency is another key feature of Corporate Bond ETFs. These ETFs disclose their holdings regularly, allowing investors to see the underlying bonds held within the portfolio. This transparency enables investors to assess the credit quality, duration, and sector exposure of the ETF, enhancing visibility and informed decision-making.

Similar to individual corporate bonds, Corporate Bond ETFs provide regular interest payments in the form of dividends to investors. These dividends are typically paid monthly or quarterly and can contribute to a steady stream of income for investors seeking yield.

Investment-grade corporate bonds are generally perceived as safer than equities

Benefits of Investing in Corporate Bonds

Investing in corporate bonds offers various advantages for investors. Firstly, corporate bonds provide a reliable source of income through regular interest payments, making them particularly attractive in low-yield environments. Secondly, adding corporate bonds into an investment portfolio enhances diversification, as they offer exposure to different industries, sectors, and credit qualities, thereby spreading risk. Furthermore, investment-grade corporate bonds are generally perceived as safer than equities, providing greater capital preservation for conservative investors seeking stable returns with lower volatility. Additionally, corporate bonds contribute to portfolio stability by mitigating the impact of market fluctuations and offering a buffer against downturns in the equity market. Finally, corporate bonds have the potential for capital appreciation, with the possibility of increasing in value if interest rates decrease or the issuer’s creditworthiness improves, thereby generating capital gains for investors.

Risks Associated with Corporate Bonds

Despite their benefits, these bonds carry inherent risks that investors should consider:

- Credit Risk: The primary risk associated with corporate bonds is credit risk, which refers to the possibility of the issuer defaulting on its debt obligations and failing to repay bondholders. Companies with lower credit ratings or financial instability are more susceptible to credit risk.

- Interest Rate Risk: Bond prices are inversely related to changes in interest rates. When interest rates rise, bond prices typically fall, and vice versa. Investors may face losses if they need to sell bonds before maturity in a rising rate environment.

- Liquidity Risk: Corporate bonds may lack liquidity, especially for less actively traded issues or during periods of market stress. Illiquid bonds may be challenging to sell at fair market prices, potentially resulting in losses for investors.

- Call Risk: Callable bonds expose investors to call risk, as issuers may redeem the bonds before maturity if interest rates decline or if the issuer’s financial condition improves. Early redemption can disrupt cash flow and limit potential returns for investors.

- Market Risk: Corporate bond prices are influenced by broader market dynamics, economic conditions, and investor sentiment. Market fluctuations can impact bond prices and yields, affecting investor returns.

Share on Social Media: